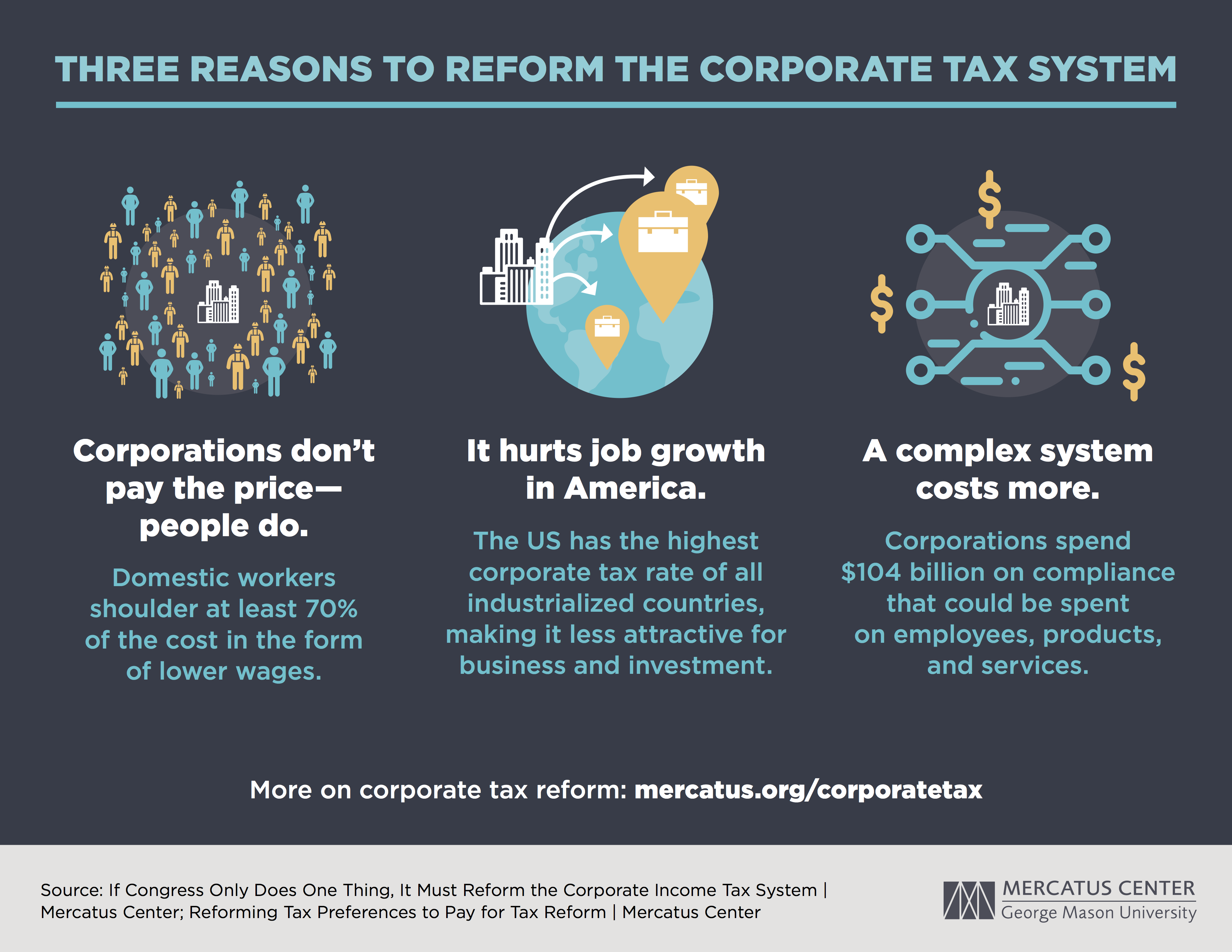

Corporate tax reform has become a central theme in the ongoing tax policy debate as the ramifications of the 2017 Tax Cuts and Jobs Act unfold. As legislators grapple with the potential expiration of key provisions from this monumental legislation, the discussion intensifies around the impacts of lowering corporate tax rates on business investment and wages. Research by Harvard economist Gabriel Chodorow-Reich sheds light on the mixed outcomes from the TCJA, highlighting increases in investment but questioning the narrative that tax cuts will inherently bolster revenue. With differing opinions emerging from both sides of the aisle, this turmoil presents a crucial moment for corporate taxation strategies moving into 2025. Such reforms could shape the future business landscape and influence how companies approach their operations and workforce in a post-pandemic economy.

The recent shifts in corporate taxation policy reflect a significant evolution in economic strategy, one that encompasses essential adjustments to business tax structures. With the foundations laid by the 2017 tax overhaul, discussions around legislative alterations are rife with implications for both financial performance and growth trajectories for businesses. The contentious climate surrounding tax reform has led to varied perspectives on the effectiveness of reduced corporate tax burdens in fostering economic prosperity and enhancing investment levels. As experts like Gabriel Chodorow-Reich analyze the trends post-Reform, the focus shifts toward how these tax adjustments not only influence corporate behavior but also affect the larger economic landscape. The ongoing discourse encapsulates the challenges faced by lawmakers as they navigate between the goals of stimulating business and maintaining sustainable government revenue.

Understanding Corporate Tax Reform

Corporate tax reform remains a contentious issue in American politics, particularly in the wake of the 2017 Tax Cuts and Jobs Act (TCJA). The TCJA significantly lowered corporate tax rates from 35% to 21%, hoping to stimulate business investments and create more jobs. However, a critical analysis by economists like Gabriel Chodorow-Reich suggests that merely slashing tax rates may not provide the anticipated economic benefits. Instead, the data reveals only a modest increase in business investments, raising questions about the efficiency and effectiveness of such tax reforms.

The implications of corporate tax reform are far-reaching, affecting both governmental revenue and economic growth. While proponents argue that lower rates encourage investment and higher wages, opponents contend that the real-world outcomes fall short of these predictions. Chodorow-Reich’s findings illustrate that while some tax cuts can foster growth, the immediate downturn in tax revenue poses substantial challenges for funding public services and programs. As part of an ongoing tax policy debate, these insights are essential for lawmakers to craft proposals that balance corporate interests with national economic priorities.

The Impact of the 2017 Tax Cuts and Jobs Act

The passage of the 2017 Tax Cuts and Jobs Act brought dramatic changes to corporate taxation in the U.S. The intention behind this landmark law was to stimulate the economy by providing businesses the impetus to invest in capital and labor. Gabriel Chodorow-Reich’s meticulous analysis indicates that the law did lead to an 11% increase in capital investments among firms. This finding contradicts some economic theories that suggest tax rates have little to no influence on business behavior, reinforcing that corporate tax policy plays a crucial role in shaping investment decisions.

Another significant aspect of the TCJA was its provision for immediate expensing of capital investments. This framework offered businesses the advantage of writing off new investments entirely within the year of purchase, effectively invigorating business spending. However, while this provision led to increased investments, the overall impact on wages proved to be modest, with estimates falling short of the ambitious projections made by the Council of Economic Advisers. This stark contrast further fuels the need for a nuanced approach toward future corporate tax reforms, particularly as lawmakers gear up for inevitable discussions regarding tax rates and incentives.

Corporate Tax Rates: A Central Issue in the Tax Policy Debate

Corporate tax rates have become a flashpoint in the ongoing tax policy debate, with passionate advocates on both sides of the aisle arguing for their preferred approach. On one end, proponents of maintaining lower corporate tax rates point to the potential for growth in business investment and job creation. On the other hand, critics argue that increasing these rates is essential to ensure that corporations contribute their fair share to government revenues, especially in the wake of revenue declines following the TCJA. This ongoing debate illustrates the complexities of designing tax policies that effectively meet the needs of both the economy and society.

Gabriel Chodorow-Reich’s research offers a valuable perspective in this debate, allowing lawmakers and stakeholders to understand the real implications of corporate tax cuts. With expectations shifting ahead of potential corporate tax reforms, insights from empirical studies reveal that any changes to corporate tax rates should be approached with caution and a thorough understanding of their potential economic impacts. The dynamics of corporate tax rates serve not only to reflect economic philosophies but also to shape the future landscape of the U.S. economy.

Business Investment and Economic Growth

The relationship between business investment and economic growth is fundamental to understanding the impacts of tax policy. The 2017 Tax Cuts and Jobs Act aimed to stimulate investment by slashing the corporate tax rate, positing that such a reduction would catalyze significant economic activity. Gabriel Chodorow-Reich’s analysis reveals, however, that the increase in business investments post-TCJA was less robust than supporters anticipated, bringing into question the effectiveness of tax cuts as an economic growth strategy.

Despite the modest improvements in investment following the TCJA, the gains were insufficient to fully offset the significant reductions in tax revenue. This disconnect highlights the need for a balanced approach that includes both tax cuts and thoughtful investment incentives. Lawmakers looking to drive economic growth must consider strategies beyond merely adjusting tax rates—focusing instead on comprehensive policies that align corporate interests with the broader economic objectives of job creation and sustainable growth.

Long-Term Effects of Corporate Income Tax Changes

The long-term effects of corporate income tax changes are a critical aspect of evaluating the success of the 2017 Tax Cuts and Jobs Act. Following the substantial reduction in corporate tax rates, economists have been tasked with examining how these changes affected corporate tax revenue and business behavior over time. Gabriel Chodorow-Reich’s insights indicate that while there was an initial 40% plunge in corporate tax revenues, many observers were surprised to see a subsequent rebound, suggesting that revenue dynamics can be more complex than immediate fiscal outcomes.

This aspect of tax reform underscores the importance of viewing tax policy as a long-term strategic tool rather than a mere short-term fix. Future policymakers should consider not only the immediate reactions within the market but also the sustained impacts on corporate behavior and fiscal health. This nuanced analysis can pave the way for more effective reforms that can boost investment without jeopardizing government revenue, ultimately creating a more resilient economic framework.

The Role of Economists in Shaping Tax Policy

Economists play a pivotal role in informing tax policy debates, providing data-driven insights that can guide legislative decisions. The work of economists like Gabriel Chodorow-Reich has become increasingly crucial as stakeholders seek to understand the implications of significant tax reforms like the 2017 Tax Cuts and Jobs Act. By analyzing empirical data pertaining to corporate tax rates and investment behavior, economists can offer clarity amid partisan disagreements and emotional rhetoric surrounding tax policies.

As lawmakers grapple with contentious issues like corporate taxation, involving economists in the dialogue can foster evidence-based discussions that lead to effective reform. Chodorow-Reich’s research illustrates the need to move beyond ideological positions and toward a more data-centric approach to tax policy. Engaging with economic analyses can help ensure that future tax legislation is well-informed and capable of achieving its intended economic effects, promoting growth without compromising fairness.

Challenges Facing Future Tax Reforms

As the expiration of key provisions from the TCJA approaches, lawmakers are bracing for another round of contentious discussions surrounding corporate tax reform. Reinstating the corporate tax rates while simultaneously renewing tax incentives for business investments poses a complex challenge for legislators. Gabriel Chodorow-Reich’s analysis helps shed light on the potential trade-offs that could emerge in this debate, where raising corporate tax rates may concurrently open up opportunities for renewed tax breaks aimed at encouraging growth.

Anticipating the political landscape leading up to 2025, it is clear that the challenges of balancing revenue generation with fostering an attractive business environment are significant. Lawmakers must prioritize comprehensive strategies that connect corporate taxes to real economic outcomes, ensuring that reforms respond to the evolving conditions of the marketplace while also addressing public needs. The resolution of these challenges will likely shape the economic landscape for years to come.

Understanding Economic Dynamics Post-TCJA

The economic dynamics following the implementation of the Tax Cuts and Jobs Act reveal the intricate relationships between tax policy, corporate behavior, and overall economic performance. Following the act’s passage, analysts observed a pattern of increased investment, which initially appeared to validate proponents’ claims regarding the benefits of tax cuts. However, Gabriel Chodorow-Reich’s findings indicate that the nuances of corporate responses to tax policy are vital to understanding broader economic implications, including labor market participation and wage growth.

As we assess the effects of the TCJA, it becomes clear that merely adjusting tax rates is insufficient for generating tangible economic gains. The post-TCJA landscape necessitates a more profound inquiry into how corporations respond to various tax incentives and the long-term effects on consumer behavior. This understanding ultimately shapes the future direction of tax reforms, influencing how lawmakers can best serve both corporate and public interests in a rapidly changing economic environment.

Future Directions in Tax Policy and Reform

Looking ahead, it’s essential for policymakers to integrate lessons learned from the TCJA into future tax reforms. The ongoing tax policy debate calls for a careful examination of the effectiveness of different strategies, including varying corporate tax rates and targeted incentives. Gabriel Chodorow-Reich’s research highlights the value of evidence-based approaches to reform, where data and economic impact assessments shape policy decisions rather than purely ideological considerations.

Adapting tax policies to reflect changing economic realities is crucial in ensuring sustainable growth and equitable revenue generation. As lawmakers prepare for the upcoming tax battles, building coalitions based on a shared understanding of economic theory and evidence can help create reforms that are both politically viable and economically sound. The combination of corporate tax reform with innovative incentives could pave the way for a more robust economic future.

Frequently Asked Questions

What are the key components of the corporate tax reform outlined in the 2017 Tax Cuts and Jobs Act?

The 2017 Tax Cuts and Jobs Act (TCJA) significantly reformed corporate taxation by reducing the corporate tax rate from 35% to 21%. Key components included immediate expensing for new capital investments, changes to business losses, and modifications to the international tax framework, aiming to encourage business investments and enhance the competitiveness of U.S. firms.

How did Gabriel Chodorow-Reich contribute to the analysis of corporate tax reform impacts?

Gabriel Chodorow-Reich, a macroeconomist at Harvard, co-authored a study analyzing the effects of the 2017 Tax Cuts and Jobs Act on corporate investments. His findings indicated that while there were modest increases in investments and wages, the cuts did not generate sufficient revenue to offset the significant losses expected from the reform.

What challenges are posed by the expiration of certain provisions in the TCJA related to corporate tax reform?

As key provisions of the TCJA are set to expire in 2025, including cuts to corporate taxes and various business incentives, there is uncertainty regarding future business investments and the overall tax policy framework. This has sparked a renewed debate in Congress about potential reforms and adjustments to corporate tax rates.

What does the recent research suggest about the relationship between corporate tax rates and business investment?

Recent research, including work by Gabriel Chodorow-Reich, suggests that corporate tax rates do affect business investment decisions. Their analysis showed that capital investments increased by approximately 11% under the TCJA, indicating that targeted tax policies can effectively drive business investments.

How have corporate tax revenues been affected since the implementation of the TCJA?

Following the implementation of the TCJA, corporate tax revenues initially fell by 40%. However, starting in 2020, these revenues rebounded significantly as corporate profits soared, often exceeding expectations, suggesting a complex interaction between tax policy and corporate performance amid changing economic conditions.

What might be the implications of raising corporate tax rates as part of potential tax reforms?

Raising corporate tax rates could provide additional revenue for federal programs but may discourage some business investments. However, economists like Gabriel Chodorow-Reich suggest that pairing rate increases with reinstating favorable expensing measures could promote growth while balancing revenue needs.

How did the 2017 Tax Cuts and Jobs Act impact wage growth according to recent studies?

Studies indicate wage growth linked to the TCJA was less significant than originally predicted. While prior estimates suggested increases of $4,000 to $9,000 per employee, research by Gabriel Chodorow-Reich and others revealed actual gains to be closer to $750 annually, demonstrating the complex effects of corporate tax reform on labor markets.

What ongoing debates exist regarding corporate tax reform in the U.S.?

Ongoing debates about corporate tax reform focus on whether to maintain or increase current corporate tax rates, the efficacy of existing incentives for business investments, and the overall impact on economic growth and equity. The partisan divide makes it a central issue in upcoming elections and legislative sessions.

| Key Points | Details |

|---|---|

| 2017 Tax Cuts and Jobs Act (TCJA) | Passed to reform outdated tax codes, reducing corporate tax rates significantly. |

| Corporate Tax Rate Reduction | Corporate tax rate cut from 35% to 21%, aiming to align with international standards. |

| Investment and Wage Impact | Investment rose about 11% due to immediate expensing provisions, but wage increases were lower than projected. |

| Political Debate | The TCJA is a major topic in upcoming elections, with debates on whether to raise or lower corporate tax rates. |

| Corporate Revenue Fluctuations | Initial drop in corporate tax revenue by 40%, but a subsequent recovery and increase noted from 2020 onwards. |

Summary

Corporate tax reform is at the forefront of political discussions as Congress prepares for a debate in 2025. The 2017 Tax Cuts and Jobs Act not only restructured corporate tax rates but also ignited significant political division regarding its effectiveness and consequences. As the expiration of provisions approaches, the future of corporate taxes remains uncertain, and analyzing past impacts is crucial for informed policymaking.